Income and Principal

Show Table of ContentsAn estate's assets are considered to consist of "principal" (the original assets themselves) and "income" (money generated by those assets and not yet spent or distributed).

Trusts are required to track principal and income separately for accounting purposes... unless a trust's governing document waives this requirement.

Estates, in contrast, can usually ignore this distinction... unless the terms of the will or a Family Entitlement specify that an heir is entitled to income generated from the estate or a particular asset (as opposed to simply giving that asset to the heir and letting the heir naturally enjoy the income it generates).

The Basics

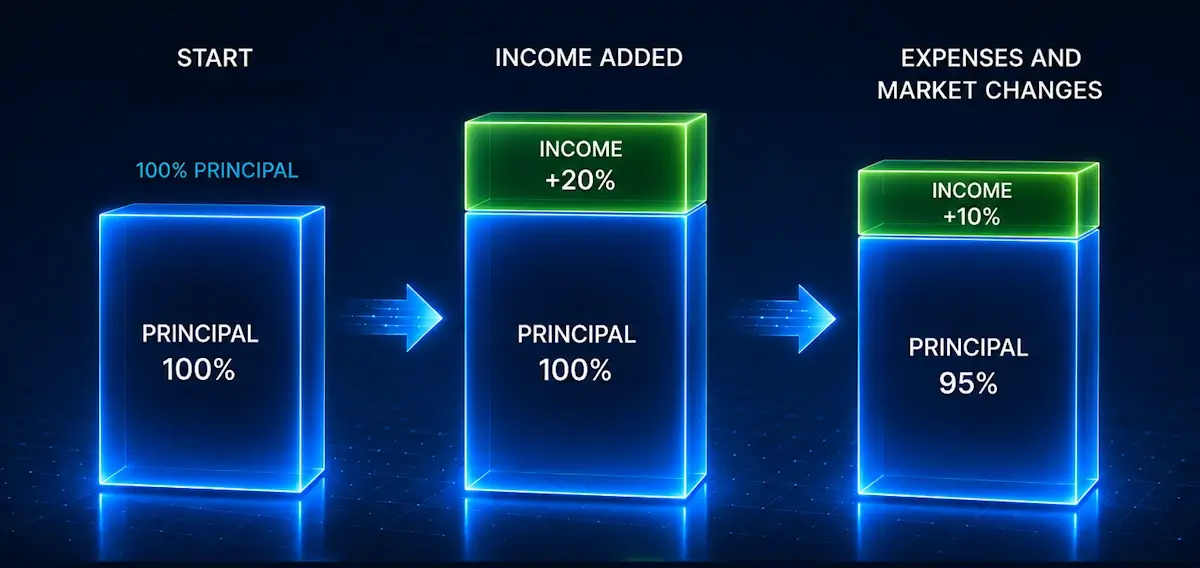

Assets are considered to be entirely principal when an estate or trust is first formed. Over time, market value changes and estate transactions (e.g., sales, capital gains distributions, debt payments) may increase or decrease that principal. Transactions may also introduce income to the estate, and may reduce that income by spending it on expenses or distributing it to heirs.

Note that from an income tax perspective, any income generated in a given year is taxed that year and then ignored in future years, but estate and trust accounting track that income forever until it is spent or distributed.

Tracking principal versus income can be more complex than it might seem, but don't worry – EstateExec will automatically handle this for you in most cases.

Tracking Changes Over Time

On the surface, it seems simple to track income and principal: you have a pool of principal that represents the assets at the start of everything, and a separate pool into which you can record deposits of income generated by those assets.

So far, so good. But what happens when you write a check for legal fees? Or pay taxes? Or deposit a capital gains distribution? What happens when you sell an asset and it has appreciated in value, maybe due to market conditions, or maybe because you spent money improving it?

A trust document (or even a will) may have special definitions or rules for determining what is considered income vs principal.

But if not, and covering any cases not explicitly handled by those documents, there are default accounting rules for almost any situation. While these rules can be complex, the following basics explain the core principles you normally need to know:

homeMarket Value Changes

Changes in an asset's market value are considered changes to principal.

homeCapital Gains Distributions

Similarly, capital gains distributions received by the estate or trust are considered principal.

money_bagTypical Income

If you are depositing interest, dividends, rent received from a tenant, or income earned from a business, you should classify these amounts as income.

money_baghomeTypical Expenses

Most estate expenses should be paid from income. If there isn't enough income to cover the expense, the remainder should be paid from principal.

homemoney_bagDebt Payments

Debt payments should be paid from principal. If there isn't enough principal to cover the debt, the remainder can be paid from income, but note that this is not a question of liquidity – if the estate has enough principal on the books to be able to cover the debt, that's how it must be recorded, even if that principal is currently tied up in something illiquid (and eventually everything will have to be balanced out).

homemoney_bagLegal Fees

Attorney fees are usually paid from principal. If there isn't enough principal, the remainder can be paid from income – but again, liquidity and availability of principal does not factor into this accounting. Separately, you do have some discretion with regards to legal fees, and if the fees were clearly related to handling income-related issues, it may be more appropriate to pay from income, or even to split the charges.

homemoney_bagAccounting and Financial Advisory Fees

Accounting and financial advisory fees are usually split 50/50 between principal and income, but you have discretion if you believe the fees are more heavily aligned with one category or the other.

homemoney_bagAsset Transfers

If you are transferring funds from one asset to another, you must preserve the combined amounts of principal and income. In other words, if you transfer the entire contents of one account to another, all income and all principal must be transferred as such. If you transfer just a portion of an account, you can decide how much of the transfer is income and how much is principal, as long as no income or principal is "created" or "lost" overall, and the total estate contains the exact same amount of income and principal as before the transfer.

homemoney_bagAsset Sales

You can look at an asset sales as simply a transfer of value from one asset (the sold item) to another (the deposit account). From this perspective, it's clear that you should preserve the ratios of the income and principal held by the sold item – and that's how EstateExec records things by default. If the sale price of an asset differs from the combined income and principal currently recorded the asset, any differences should be attributed to principal.

However, it's also common practice to treat the entire proceeds as principal, so there can be some judgment applied here, as well as some situational accounting black magic.

homemoney_bagExecutor and Trustee Fees

Executor and trustee fees should be paid 50% from income, and 50% from principal... to the extent possible. In practice, that means that if you don't have enough income to cover 50%, the rest should come from principal. And if you don't have enough principal (in total, ignoring any liquidity concerns), the rest should come from income... which would be a rare situation.

Distributions

Classification of distributions into income and principal depends on the nature of the distribution and the nature of the asset:

homemoney_bagBequest Distributions

Bequest distributions are generally considered principal. A bequest of a piano is principal. A bequest of $10,000 is principal.

However, if a bequest is made of an asset that generates income after the death and before being actually distributed, then the distribution will include that corresponding income (minus any expenses that asset has also incurred in the meantime, since expenses usually pull first from income).

And if the bequest is income by definition, then naturally it is considered income for estate accounting – for example, if the will leaves an heir the income from a particular asset for 10 years or for life.

homemoney_bagResiduary Distributions

Residuary distributions include everything that's left over at the end: whatever mix of principal and income exists.

Handling Asset/Estate Differences

The notion of income and principal applies to transactions, assets, and the estate or trust overall. If you have consolidated everything into a single bank account, everything is easy and straighforward.

But if you have several assets, with varying mixes of income and principal, and then want to pay something out of a particular asset, it can be confusing if the transaction should be paid from income (for example), and while the estate overall contains enough income to fund the transaction, the asset from which you want to write the check does not.

How you should handle such a case depends on the circumstances. For example:

- If you are writing an income distribution check that is supposed to be funded by that particular asset, you might want to wait until the income actually becomes available, or potentially reduce the amount of the check.

- If there are no complications concerning prior claims on asset income or principal, and it's just a general administration expense, you might want to first transfer income from another asset so that you can properly fund the check. You don't necessarily need to move funds around in the real world – you can instead simply record an income transfer from an asset that has the needed income, and record a reverse transfer of principal.

- If it's just a temporary situation, you might want to just go ahead with the full allocation to income, recording a negative income balance for the given asset, with the understanding that this will need to be made whole at some point.

Ultimately, you will have to use your judgment to ensure that everything is handled appropriately, that neither income nor principal is inadvertantly transmuted into the other, and that estate and trust obligations are met in their priority order.

Priorities

If certain estate heirs or trust beneficiaries are entitled to receive only income, and others only principal, you will need to pay extra attention to the differentiation between income and principal.

For example, should you manage assets and invest to maximize short-term income or long-term capital appreciation? For many estates, this question is somewhat irrelevant, as the executor's job is to expeditiously settle the estate, and in the short term the priority is simply to avoid catastrophic loss while still maintaining reasonable returns.

If you are dealing with a more long-term situation, however, these tradeoffs can become important, and you usually need to ensure you are not maximizing one group's results over another's.

Complex Situations

Income and principal accounting can get rather convoluted in complex edge cases (e.g., accrued bond interest held less than a year, investment funds in which income versus principal return information is not available, depreciation and amortization, etc.). If you think your trust (or estate) needs to account for such things, you should seek the help of a qualified accountant.

Tax Implications

As mentioned above, income tax accounting focuses on net income generated in a given tax year, while estate and trust (e.g., fiduciary) accounting tracks income forever until it is spent or distributed.

There are other key differences. In particular, income tax accounting assumes any distributions in a given year come first from any available income, only dipping into principal after all income from that year has been exhausted (this is especially important for trusts, as the burden for paying taxes on that income shifts to anyone who receives a portion of that year's income). Consequently, a trust could report to heirs that it distributed a bequest of principal, while simultaneously reporting that from an income tax perspective, that distribution must be considered income.